Owner Earnings Give Truer Sense of a Company’s Cash Generation

Owner Earnings Give Truer Sense of a Company’s Cash Generation

Accounting figures should serve investors, not rule them.

“Markets will change significantly - you can be sure of that and some day we will again get our turn at bat. However, we haven’t the faintest idea when that might happen.” - Buffett

This week we’re going to walk through an important and lengthy discussion about owner earnings, an idea for which Buffett is very well-known. Owner earnings can be thought of as the cash generated by a business that’s available to owners after accounting for maintenance costs. It more or less corresponds with the concept of free cash flow. Buffett gives a detailed example of how he thinks about owner earnings in his 1986 letter, which involves examining the income statement and balance sheet of Scott Fetzer, a business Berkshire acquired in ‘86 for $315M.

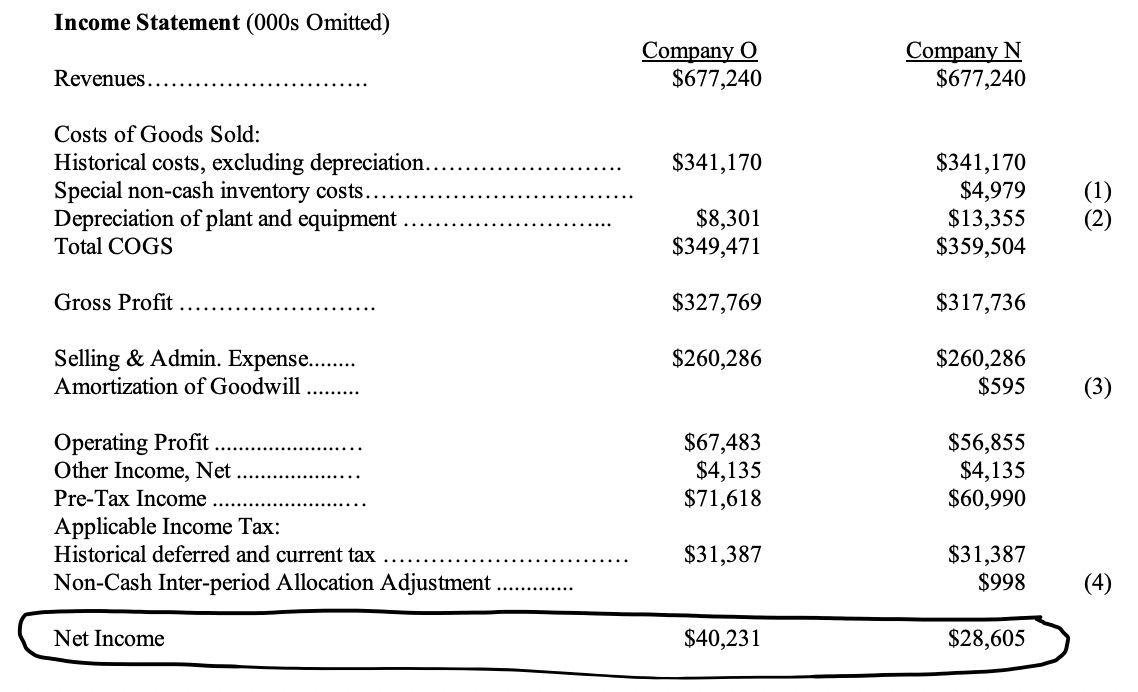

Buffett starts by posing a question: looking at the income statements of the following two companies, which is more valuable?

Turns out, Company O and N are the same business, only the accounting is different. Company O (old) represents Scott Fetzer’s ‘86 earnings sans being acquired, and Company N (new) represents Fetzer’s GAAP earnings as reported by Berkshire after the acquisition. Knowing the companies are identical, Buffett asks, “Upon which set of numbers should managers and investors focus?”

The question is relevant because if we use O’s earnings, Berkshire paid 7.8 times earnings for Fetzer (315M/40.2M = 7.8), but if we use N’s earnings, Berkshire paid 11x earnings (315M/28.6M = 11).

To answer this, we first have to look at how the disparity arises.

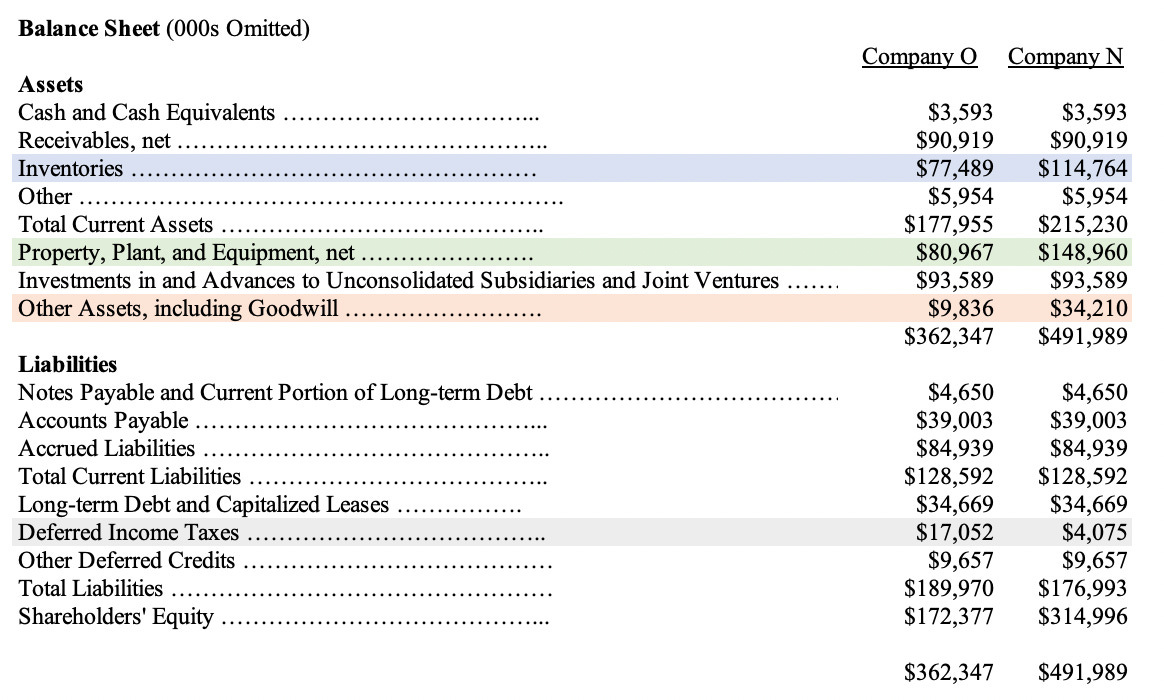

When a business is acquired, there is usually a premium or discount paid to the net asset value of the company.1 Fetzer’s net asset value at the time of acquisition was $172.4M (see O’s balance sheet below). Berkshire paid $315M for the business, or a $142.6M premium to net asset value. To account for this difference and reconcile the new balance sheet, a series of “purchase-price adjustments” are required.

We don’t need to get bogged down in the specificities of these adjustments. Generally, it includes adjusting the carrying value of current & non-current (or fixed) assets and current & non-current liabilities to their current value. For example, it was determined that Fetzer’s inventories were carried at a $37.3M discount to current value. Thus, post-acquisition Company N’s inventories are increased by $37.3M to $114.7M (highlighted in blue). Thus, $37.3M of the $142.6M premium that Berkshire paid has been reconciled, leaving a $105.3M to still be accounted for. A similar accounting move is performed with the carrying value of Fetzer’s property, plant, and equipment (PPE), resulting in $68M being added to Company N’s assets, bringing PPE to $149M (highlighted in green).

Deferred income taxes are adjusted, reducing liabilities by $13M (highlighted in gray).

The last item is a catchall. After adjusting any eligible figures, the remaining purchase price premium is allocated to Goodwill - in this case, $24.3M (highlighted in orange). Goodwill is defined as the "excess of cost over the fair value of net assets acquired.” In layman terms, Goodwill can be thought of as the value of a business’ brand that can’t be easily captured or quantified on paper.

At this point, the $146.2M purchase price premium has been fully accounted for on the balance sheet. The larger balance sheet figures for N results in a lower net income figure for N. The reason is because the written-up assets must be depreciated and amortized. Thus, the greater the asset value, the greater the annual depreciation and amortization charge to earnings.

The charges that flowed to the income statement due to the write-ups on the balance sheet are numbered below:

(1) represents a charge for special non-cash inventory costs.

(2) increased depreciation charge against PPE due to the higher asset values. PPE is depreciated on a straight line over the course of the useful life of the asset.

(3) increased amortization charge against the $24.3M allocated to Goodwill with the acquisition. Amortization simply refers to the depreciation of intangible assets.

(4) represents a one-off non-cash adjustment.

All in, the result is a $11.6M charge to the income statement, reducing GAAP earnings from $40.2M to $28.6M. At this point, Buffett returns to his question:

What does all this mean for owners? Did the shareholders of Berkshire buy a business that earned $40.2 million in 1986 or did they buy one earning $28.6 million? Were those $11.6 million of new charges a real economic cost to us?...If a business is worth some given multiple of earnings, was Scott Fetzer worth considerably more the day before we bought it than it was worth the following day?

Buffett says no, and introduces the concept of owner earnings to explain why:

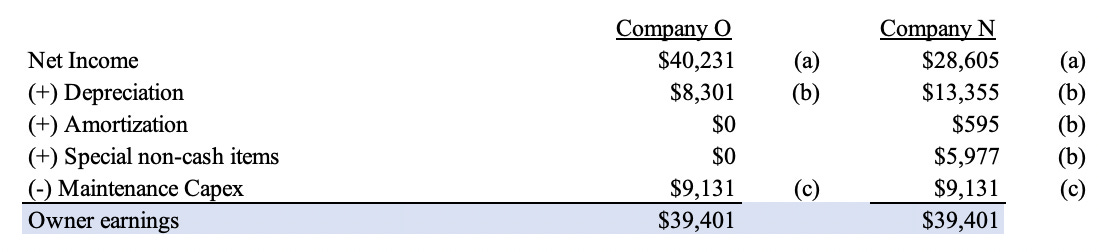

If we think through these questions, we can gain some insights about what may be called "owner earnings.” These represent (a) reported earnings plus (b) depreciation, depletion, amortization, and certain other non-cash charges such as Company N's items (1) and (4) less (c) the average annual amount of capitalized expenditures for plant and equipment, etc. that the business requires to fully maintain its long-term competitive position and its unit volume. (If the business requires additional working capital to maintain its competitive position and unit volume, the increment also should be included in (c).2

Item (c) can be thought of as maintenance capex, or the portion of total capex that is required for a business to retain its competitive position and unit volume. Capex in excess of maintenance is considered growth capex, and is deployed to expand unit volume or gain market share. Given the company is not required to spend this to maintain its current position, it’s not deducted from owner earnings. Meaning, instead of reinvesting the cash for growth, management could elect to instead distribute it to shareholders through dividends or share buybacks.

We can now plug Company O and N’s values into the owner earnings equation, arriving at a figure that is identical for both companies. While maintenance capex (item c) is an estimate, it definitionally must be the same for O and N because they’re the same business. You’ll notice that owner earnings approximates a free cash flow metric that many investors use today.3

Owner earnings are not as precise as GAAP earnings because item (c) must be estimated4. However, Buffett argues they’re more representative of the business because they strip out accounting idiosyncrasies:

Our owner-earnings equation does not yield the deceptively precise figures provided by GAAP, since (c) must be a guess - and one sometimes very difficult to make. Despite this problem, we consider the owner earnings figure, not the GAAP figure, to be the relevant item for valuation purposes - both for investors in buying stocks and for managers in buying entire businesses. We agree with Keynes's observation: ‘I would rather be vaguely right than precisely wrong.’

What is an appropriate estimate for maintenance capex? For physical asset-intense businesses, depreciation is generally a good proxy for maintenance capex, although it often understates it5. Thus, for the sake of illustration, in the above table I assumed maintenance capex was 110% of Company O’s depreciation charge.

Below is Buffett explaining:

And what do Charlie and I, as owners and managers, believe is the correct figure for the owner earnings of Scott Fetzer? Under current circumstances, we believe (c) [maintenance capex] is very close to the "old" [O] company's (b) number of $8.3 million and much below the "new" [N] company's (b) number of $19.9 million.”

The lesson for Buffett in all of this is that GAAP figures are meant to serve investors and managers, not rule them.

Questioning GAAP figures may seem impious to some. After all, what are we paying the accountants for if it is not to deliver us the "truth" about our business. But the accountants' job is to record, not to evaluate. The evaluation job falls to investors and managers. Accounting numbers, of course, are the language of business and as such are of enormous help to anyone evaluating the worth of a business and tracking its progress...Managers and owners need to remember, however, that accounting is but an aid to business thinking, never a substitute for it.

Net asset value is equal to Assets less Liabilities, or Shareholders’ Equity.

If additional working capital is required to maintain its competitive position and unit volume, this should also be included in (c).

I’m not sure how Buffett would treat stock-based compensation, which increasingly accounts for a large percentage of software companies’ free cash flow because it’s deducted as a non-cash expense. My guess is he would exclude it.

While some do, most companies don’t disclose the portion of capex that is designated for maintenance purposes.

Hi David, thank you for this great post! (I hope you can still read this comment)

I went to Mauboussin's paper on MCX vs. GCX [amazing btw] and what shocked me was that FCF is defined as NOPAT - Investment for growth which eliminates the MCX, whereas Owner's earnings only consider MCX. Thus, I tried to conclude that FCF is a good tool for a discounted present value model and Owner's earnings is more for peer comparison. What are your thoughts about it? Am I mistaken on the fact that FCF only considers GCX?

From the paper — "Free cash flow, the number we project and discount in a discounted-cash flow model, is typically defined as net operating profit after taxes (NOPAT) minus investment in future growth (I). Investment in future growth captures changes in net working capital, as companies often need to increase their working capital as they grow, and capital expenditures net of depreciation. The simplifying assumption is that depreciation is a reasonable proxy for maintenance capital spending and that investment in excess of depreciation is allocated to growth."